Embark on a journey to understand How to Compare Small Business Health Insurance Plans. This guide will unravel the complexities and provide insights for small business owners seeking the best health insurance options.

Delve into the intricacies of coverage options, costs, pricing structures, and network coverage to make informed decisions that benefit both the business and its employees.

Researching Small Business Health Insurance Plans

When it comes to selecting the right health insurance plan for your small business, thorough research is key to making an informed decision. By exploring various options, you can find a plan that meets the needs of your employees while staying within your budget.

Key Factors to Consider

- Cost: Compare premiums, deductibles, copayments, and coinsurance to determine the overall cost of the plan.

- Coverage: Evaluate the services covered, such as doctor visits, prescription drugs, and preventative care.

- Network: Check if your preferred healthcare providers are in-network to ensure accessible care for your employees.

- Flexibility: Consider the ability to customize the plan to accommodate the unique needs of your workforce.

- Customer Service: Look for feedback on the insurer’s responsiveness and support to address concerns efficiently.

Resources for Information

Small business owners can explore the following resources to gather information on available health insurance plans:

- Healthcare.gov: Offers a marketplace where you can compare different plans and learn about eligibility requirements.

- Insurance Brokers: Consult with a broker specializing in small business health insurance to get personalized recommendations.

- Chamber of Commerce: Local chambers often provide resources and guidance on health insurance options for small businesses.

Understanding Coverage Options

When choosing a small business health insurance plan, it’s crucial to understand the different coverage options available. These options can vary based on the needs of your business and its employees, so it’s important to carefully consider each one.

Types of Coverage Options

- Health Maintenance Organization (HMO): Typically requires employees to choose a primary care physician and get referrals to see specialists.

- Preferred Provider Organization (PPO): Offers a network of providers for employees to choose from, with the option to see out-of-network providers at a higher cost.

- High Deductible Health Plan (HDHP): Requires employees to pay a higher deductible before the insurance kicks in, often paired with a Health Savings Account (HSA).

Essential Health Benefits

- Preventive care services: Including vaccinations, screenings, and annual check-ups.

- Emergency services: Coverage for emergency room visits and ambulance services.

- Prescription drug coverage: Assistance with the cost of medications.

Varying Coverage Based on Needs

Different businesses have different needs when it comes to health insurance coverage. For example, a business with a younger workforce may prioritize preventive care services and prescription drug coverage, while a business with older employees may focus on coverage for chronic conditions and specialist care.

It’s essential to tailor your coverage options to meet the specific needs of your business and employees.

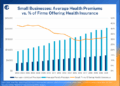

Comparing Costs and Pricing Structures

When comparing small business health insurance plans, it’s crucial to understand the different cost components involved to make an informed decision that meets both your budget and coverage needs.

Cost Components in Small Business Health Insurance Plans

- Premiums: These are the monthly payments you make to the insurance company to maintain coverage.

- Deductibles: The amount you must pay out of pocket before your insurance starts covering costs.

- Copayments: Fixed amounts you pay for healthcare services or prescriptions at the time of service.

- Coinsurance: The percentage of costs you are responsible for after meeting your deductible.

Pricing Structures

- Indemnity Plans: Offer the most flexibility but tend to have higher premiums.

- Health Maintenance Organizations (HMOs): Require you to choose a primary care physician and get referrals for specialists.

- Preferred Provider Organizations (PPOs): Offer more flexibility in choosing healthcare providers but often come with higher premiums.

Evaluating Costs for an Affordable Plan

- Assess your budget and determine how much you can afford to spend on premiums, deductibles, and copayments.

- Compare plans based on total costs, including monthly premiums and out-of-pocket expenses.

- Consider the coverage and benefits provided by each plan to ensure it meets your healthcare needs.

Evaluating Network Coverage and Providers

When choosing a small business health insurance plan, evaluating network coverage and providers is crucial to ensure that employees have access to quality healthcare services when needed.

Network coverage refers to the group of healthcare providers, such as doctors, specialists, hospitals, and clinics, that have contracted with the insurance company to provide services at a discounted rate to plan members. The network can impact the cost of care, the ease of accessing services, and the quality of care received.

Assessing Healthcare Provider Networks

Before selecting a health insurance plan, it’s essential to assess the network of healthcare providers included in the plan. Here are some steps to help you evaluate the network:

- Check if your current healthcare providers are in-network to continue receiving care from them.

- Review the list of in-network providers to ensure there are enough options in your area and specialties needed.

- Consider the distance to in-network providers to ensure they are conveniently located for employees.

- Check if the plan offers out-of-network coverage in case employees need to see providers who are not in-network.

Benefits of In-Network vs. Out-of-Network Providers

Understanding the benefits of using in-network providers versus out-of-network providers can help you make informed decisions about network coverage:

- In-Network Providers:Typically cost less, have pre-negotiated rates with the insurance company, and offer better coverage for services.

- Out-of-Network Providers:May cost more, require higher out-of-pocket expenses, and may not be covered fully by the insurance plan.

- Using in-network providers can help employees save money and ensure they receive the full benefits of their health insurance plan.

Final Review

In conclusion, navigating the realm of small business health insurance plans requires careful consideration and evaluation. By understanding the key factors and details discussed, you can confidently choose a plan that meets your business needs effectively.

Popular Questions

What are the key factors to consider when comparing small business health insurance plans?

Key factors include coverage options, costs, pricing structures, and network coverage.

How can small business owners find information on available health insurance plans?

Small business owners can research online, consult insurance brokers, or contact insurance providers directly.

Why is network coverage important in a health insurance plan?

Network coverage determines which healthcare providers are included and affects the accessibility of healthcare services.

{kind=link}